-

Estimated vs. Actual Earnings: BAC reported an adjusted EPS of $0.83, slightly above the estimated $0.77.

-

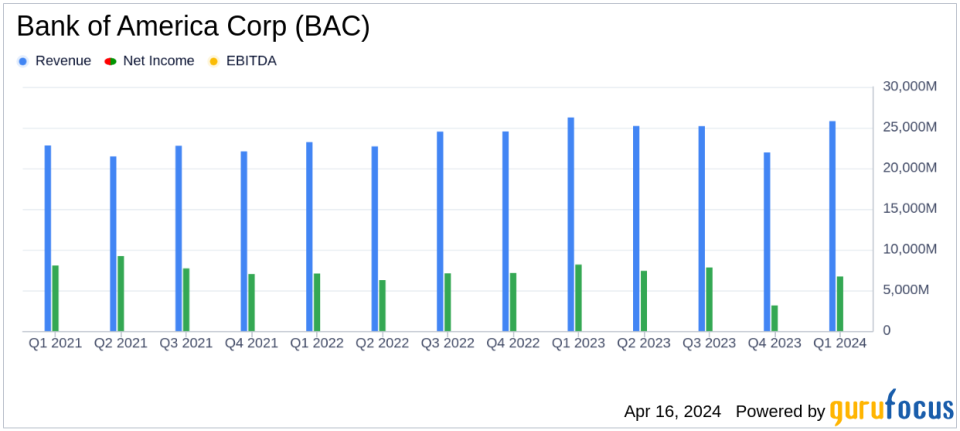

Estimated vs. Actual Net Income: Reported net income was $6.7 billion, falling short of the estimated $6.229 billion.

-

Estimated vs. Actual Revenue: Revenue aligned with analyst projections, totaling $25.8 billion.

-

Provision for Credit Losses: Increased to $1.3 billion from $931 million in Q1-23.

-

Net Charge-Offs: Rose to $1.5 billion, up from $807 million in Q1-23.

-

Return on Average Assets (ROA) and Equity (ROE): ROA stood at 0.83%, with ROE at 9.4%.

On April 16, 2024, Bank of America Corp (NYSE:BAC) released its 8-K filing, revealing a quarter that saw a mix of achievements and challenges. BAC’s adjusted earnings per share (EPS) of $0.83 exceeded analyst estimates of $0.77, while net income of $6.7 billion fell short of the expected $6.229 billion. The company’s revenue aligned with projections, coming in at $25.8 billion.

Bank of America is a leading financial institution in the United States, with a significant presence in consumer banking, wealth management, global banking, and markets. Its diverse range of services includes retail lending products, brokerage, investment banking, and capital markets operations, primarily focused on the U.S. market.

The quarter’s performance reflected a decrease in net interest income due to higher deposit costs, which overshadowed higher asset yields and modest loan growth. The provision for credit losses increased to $1.3 billion, up from $931 million in the same quarter of the previous year. This was attributed to a net reserve release of $179 million, compared to a net reserve build of $124 million in Q1-23. Net charge-offs also increased to $1.5 billion, up from $807 million in Q1-23.

Noninterest expense rose to $17.2 billion, a 6% increase, primarily due to a special FDIC assessment. Excluding this, the adjusted noninterest expense was $16.5 billion, a 2% rise. The company’s efficiency ratio, a measure of noninterest expense as a percentage of revenue, was 67%, showing an increase from the previous year’s 62%.

From a balance sheet perspective, average deposit balances grew to $1.91 trillion, with a 1% increase in average loans and leases to $1.05 trillion. The CET1 capital ratio remained strong at 11.8%, comfortably above the regulatory minimum.

Chair and CEO Brian Moynihan highlighted the strong quarter performance, noting the growth in consumer checking accounts and wealth management revenue, as well as a rebound in investment banking. The sales and trading business also saw its best first quarter in over a decade, contributing to the company’s overall performance.

Despite the mixed financial outcomes, Bank of America Corp (NYSE:BAC) demonstrated robust business segments and continued digital engagement growth. The company’s ability to navigate economic headwinds while maintaining a strong capital position and delivering value to shareholders underscores its resilience in a challenging environment.

For more detailed insights and financial analysis, investors are encouraged to visit GuruFocus.com for comprehensive reports and expert commentary.

Explore the complete 8-K earnings release (here) from Bank of America Corp for further details.

This article first appeared on GuruFocus.